Will Social Security Be Around in Ten Years? What Federal Employees Should Know

It’s a question on the minds of millions of Americans: Will Social Security still be around when it’s my time to use it? As the headlines grow more urgent and the 2030s inch closer, concerns about the longevity of Social Security are no longer reserved for distant retirement conversations, but a topic to begin addressing with your financial professional now.

If you're a federal employee, especially one under the Federal Employees Retirement System (FERS), Social Security represents one leg of your three-part retirement stool, along with your Thrift Savings Plan (TSP) and FERS annuity. Understanding the health and future of your retirement picture is an essential part of your long-term financial planning.

Let’s take a closer look at how Social Security works, why people are concerned, and what you can do to protect your financial future regardless of politics or economic impact.

How Is Social Security Funded?

Social Security is not some static pot of money waiting in your individual account ready to pay out when it’s your time to collect. It’s a pay-as-you-go system, which means that payroll taxes collected from current workers fund the benefits paid out to current retirees. The system is funded in two ways:

- FICA taxes: 6.2% from employees and 6.2% from employers (including the government), totaling 12.4% for Social Security.

- Self-employment tax: For contractors or those with side businesses, it’s 12.4% in total, though half is deductible.

When Social Security collects more than it pays out, the surplus is invested in special-issue Treasury securities, which is a form of trust fund savings. But here’s where the concern starts: that surplus is shrinking.

The State of the Trust Fund

According to the 2024 Social Security Trustees Report, the combined reserves of the Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) Trust Funds are projected to be depleted by 2033. At that point, the program would rely solely on incoming payroll taxes, which are projected to cover only 77% of scheduled benefits.

Think of Social Security like a water tank that’s constantly being filled by workers pouring in buckets (payroll taxes) and drained by retirees using faucets (benefits). Right now, more water is being drained than poured in, and unless we slow the faucets or add more buckets soon, the reserve tank will be depleted, only sending out exactly what has been dumped in each year.

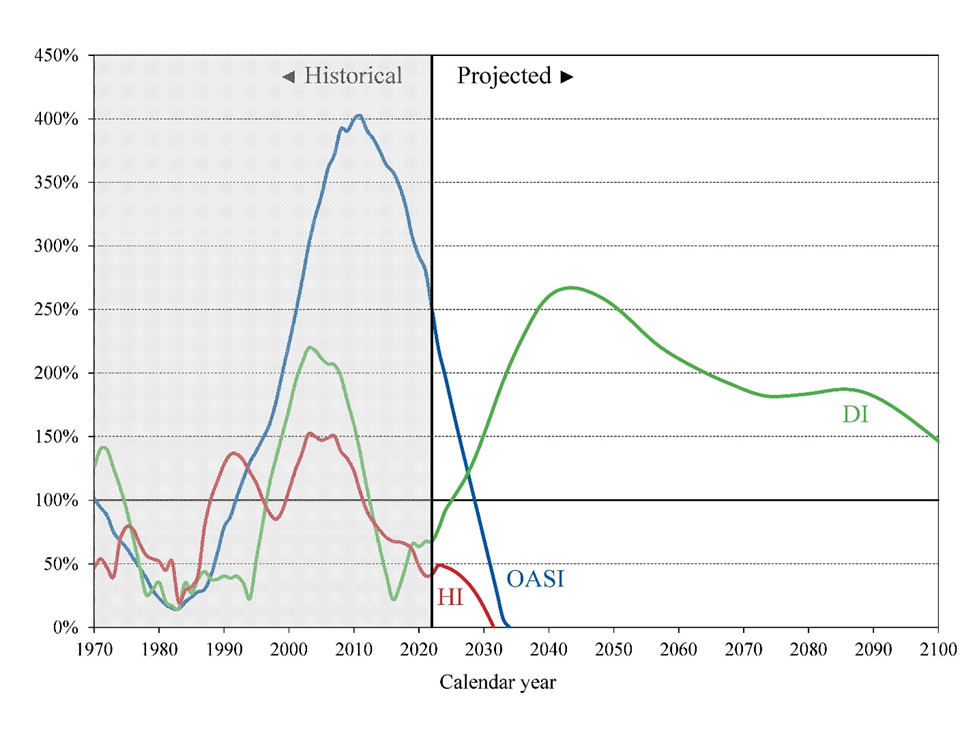

The chart below from the Social Security Administration’s 2023 Annual Trustees Report shows the growth and projected decline of Social Security trust fund reserves (OASI and DI) through the mid-2030s.

To be clear, this does not mean Social Security would vanish overnight, as the chart suggests. It means that if Congress does nothing to support the system, there will be no surplus left to sustain the oversized outflows. If this happened, the benefits being paid out would have to equal the contributions being paid in. This would reduce current benefit projections by about 23%.

That’s a big “if,” and many experts believe reforms will happen before the system reaches that point. It’s vital to understand what’s at stake, and what you can do now to be prepared. Let’s start by understanding why this is happening.

Why Is Social Security Depleting So Fast?

Several factors contribute to the financial squeeze:

- Aging population: Baby boomers are retiring in droves, and people are living longer. That means more people are drawing benefits for a longer time.

- Lower birth rates: Fewer workers are entering the workforce to replace retirees, weakening the ratio of workers to beneficiaries.

- Wage stagnation and income inequality: High-income earners contribute a smaller percentage of their income to Social Security due to the taxable earnings cap.

In short, the system was designed in the 1930s under very different demographic assumptions. While it has been updated over the years, the speed and scale of today’s changes demand more aggressive reforms.

What Happens If the Trust Fund Runs Dry?

If Congress takes no action and the trust fund is depleted:

- Reduced benefits: As mentioned, retirees could see automatic cuts of about 23%, which could increase over time.

- Impact on federal employees: For FERS-covered employees, Social Security makes up about 30-40% of your projected retirement income. A reduction would be significant, particularly for those relying on it to cover essential living expenses.

- Increased pressure on personal savings: You may need to lean more heavily on your TSP or personal investments to make up the difference.

It’s important to note that Congress has options to prevent this scenario, including raising the taxable wage cap, increasing the retirement age, adjusting benefits formulas, or increasing payroll taxes.

Facing the Future with Confidence

Here’s what we do know: even in the worst-case scenario, Social Security won’t disappear. The program would continue to exist and pay benefits, even though it’ll be at a reduced rate. Historically, Congress has acted before allowing massive reductions to kick in. In fact, reforms in 1983, after a similar funding crisis, were enacted just in time to stabilize the system for decades.

That said, counting on Congress to save the day is not a substitute for a proactive retirement plan. If you're feeling uncertain about your retirement future, you're not alone. Rather than reacting with worry, let this uncertainty inspire you to take active steps toward financial confidence.

Now may be a great time to be proactive about your future by working with a trusted financial professional who can help you:

- Assess your retirement plan: They can help you understand how changes, such as a reduction in Social Security benefits, could impact your income and suggest ways to adjust your strategy accordingly.

- Optimize savings and investments: Whether it’s your workplace retirement plan, personal savings, or other investments, you can receive professional guidance tailored to your unique goals and risk tolerance.

- Enhance tax efficiency: They can help you navigate the complexities of withdrawals and distributions, aiming to minimize taxes and help your savings last longer.

- Stay informed: Financial professionals keep up with legislative and economic changes, so you receive relevant, timely advice without having to track every detail yourself.

- Prepare for the unexpected: From shifts in government programs, such as Social Security, to market volatility or rising healthcare costs, can help you anticipate challenges and adapt your plans proactively.

As a federal employee, you’ve dedicated your career to serving the public. You deserve a secure and stable retirement. Social Security may be facing challenges, but the sky is not falling. Still, relying blindly on benefits that may shift is a risk no one can afford to take lightly.

Work with someone who understands the nuances of federal benefits, the uncertainties of the current system, and how to help you craft a retirement plan that’s flexible, resilient, and tailored to your needs.

Just because a specific payout benefit like Social Security may change, your retirement plan doesn’t have to.

Neil Cain and Austin Costello are certified financial planners with Capital Financial Planners. If you have questions about how retirement impacts your Medicare payments, register for a complimentary checkup. For topics covered in even greater depth, see our YouTube page.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Securities and financial planning offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC