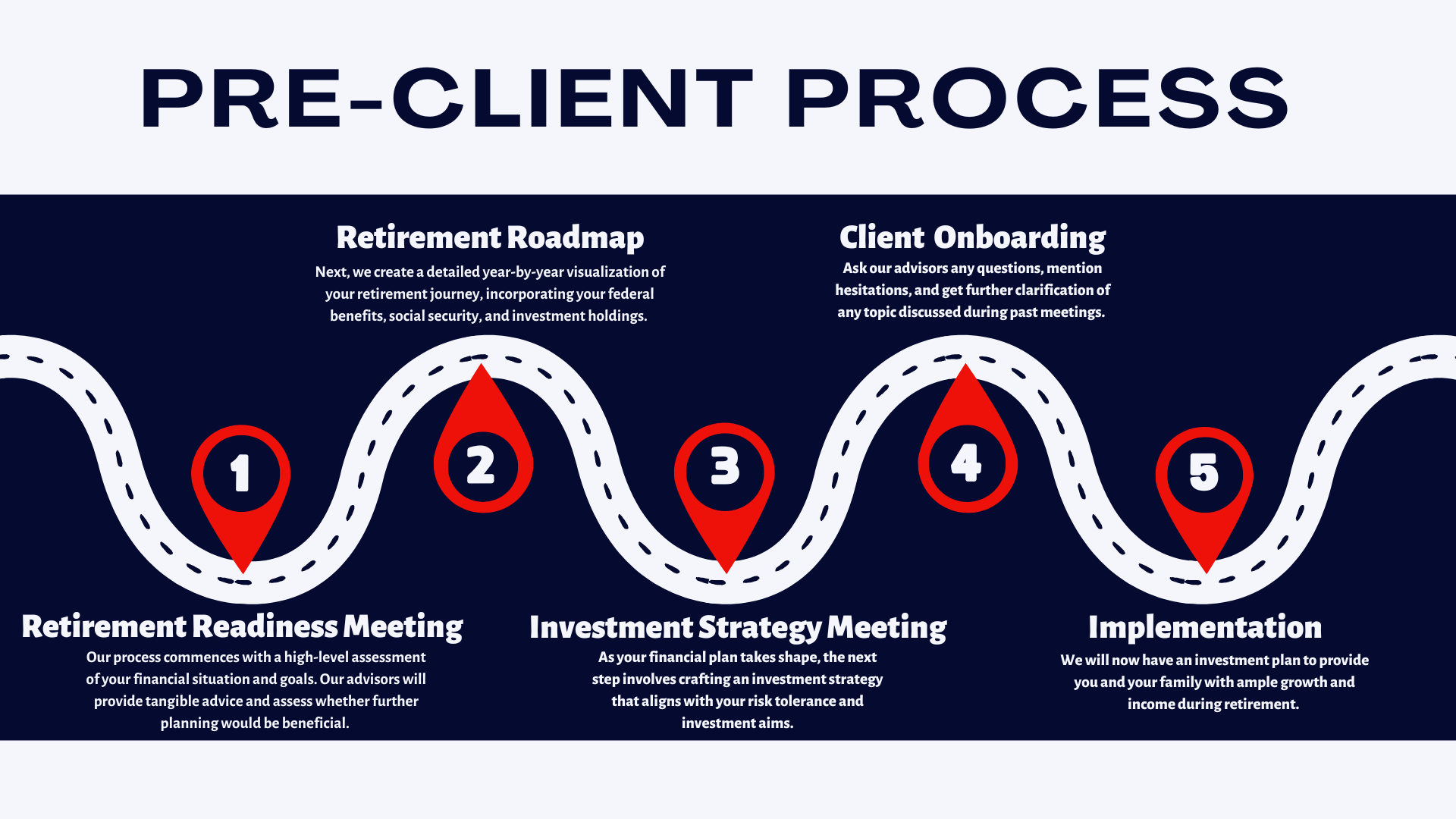

For more information on our Retirement Roadmap Analysis, please click here.

For additional questions, please visit our Prospective Client FAQ page.

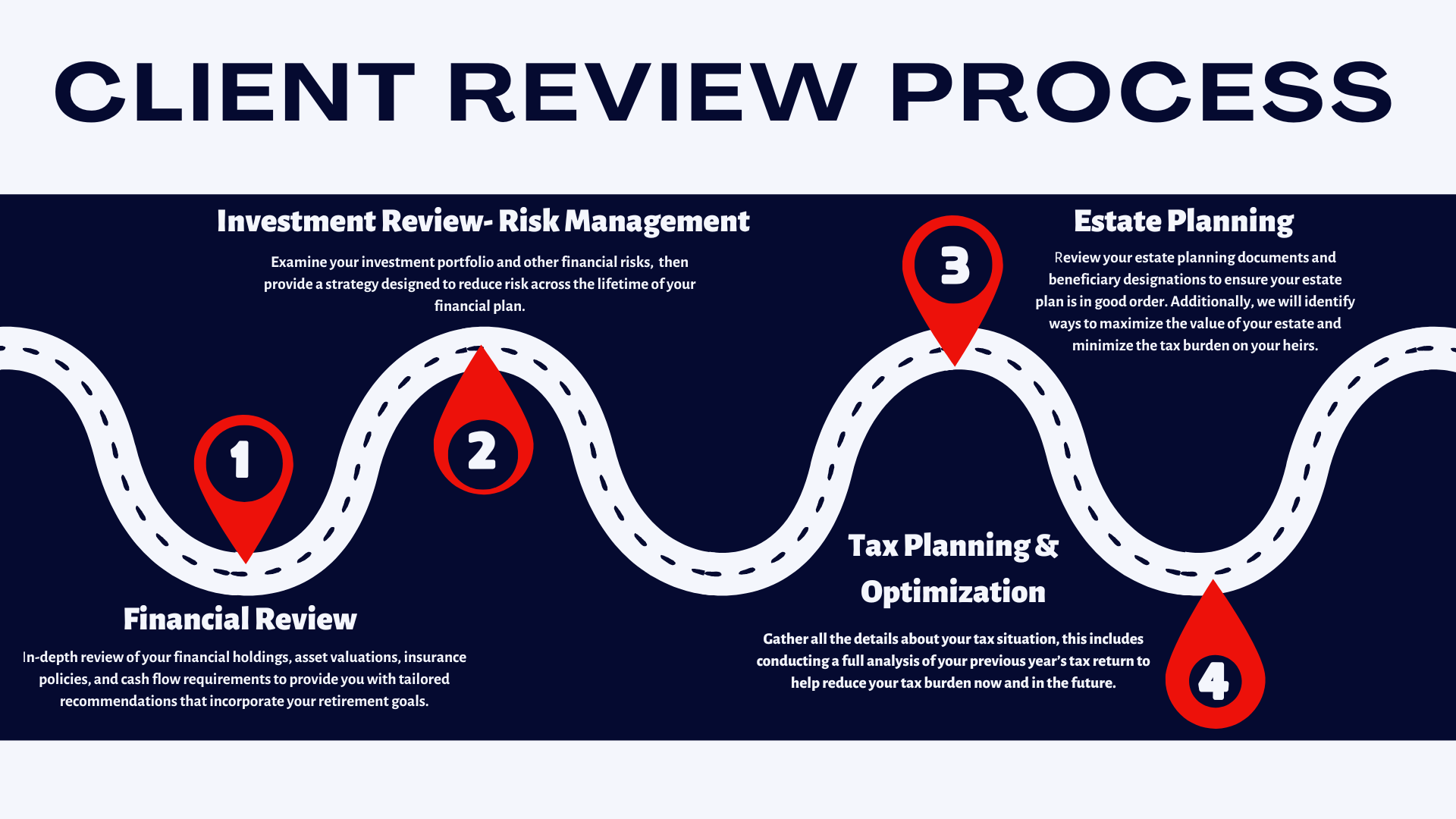

Please click here to visit our Prospect Corner for more information.

For additional questions, please visit our Prospective Client FAQ page.

Please click here to visit our Prospect Corner for more information.

Click here to schedule a Financial Checkup to see if our Retirement Roadmap Analysis is for you.